Why Commerce Needs Its Own Blockchain

A 3-second finality thesis, grounded in numbers.

The Neighborhood Tax

There's a pupusería in Silver Spring, Maryland, that has been open since 2014. The owner — call her Maria — makes everything from scratch. On a good month she does about $10,200 in gross revenue through DoorDash. Last month, DoorDash kept $2,247 of it.

Twenty-two percent. Not for ingredients, not for labor, not for rent — for visibility. She pays it because the alternative is worse: three blocks away, a Chipotle with a corporate ad spend doesn't need DoorDash to show up in search results. Maria does.

Across the United States, sole proprietors share anywhere from 15–30% of their revenue with marketplace platforms just to participate in the online economy. Add the payment processing fee underneath — 2.9% + $0.30 on every card transaction — and a $38 delivery order might net the restaurant $24.

Every layer between the customer's intent and the merchant's register extracts a toll. The card network takes its interchange. The processor takes its margin. The platform takes its commission. The merchant gets what's left. The smallest operators pay the highest effective rate. The system is regressive by design.

Now look at this from a pure infrastructure perspective.

A coffee shop in Portland processes a $4.50 latte on its card terminal. The customer taps, sees a checkmark, and walks away. Visa authorizes that transaction in approximately 1.8 seconds — but authorization is not settlement. The merchant won't see those funds for 1–2 business days.

That tap flows through a payment processor — Square, Stripe, Toast — each layering fees on the base interchange rate. On a $4.50 latte, the merchant pays roughly $0.17–$0.26 in processing fees at the register. For online commerce, processor fees climb to 2.9% + $0.30 per transaction — nearly 10% of a small purchase. Add chargebacks, PCI compliance costs, and platform fees, and the real cost of card acceptance far exceeds the headline interchange rate.

Card networks are not the gold standard. They are the incumbent — fast at the point of sale, but expensive, opaque, and gated behind intermediaries.

Now try the same thing on a blockchain.

On Ethereum, the customer waits 12–15 seconds for a single block confirmation. The gas fee might exceed the purchase price during congestion. On Solana, latency is better (~400ms slot time), but fee spikes during high demand can make small transactions economically irrational.

Neither legacy payment rails nor existing blockchains deliver what commerce actually needs: sub-3-second finality, sub-cent fees, and direct merchant settlement without intermediaries.

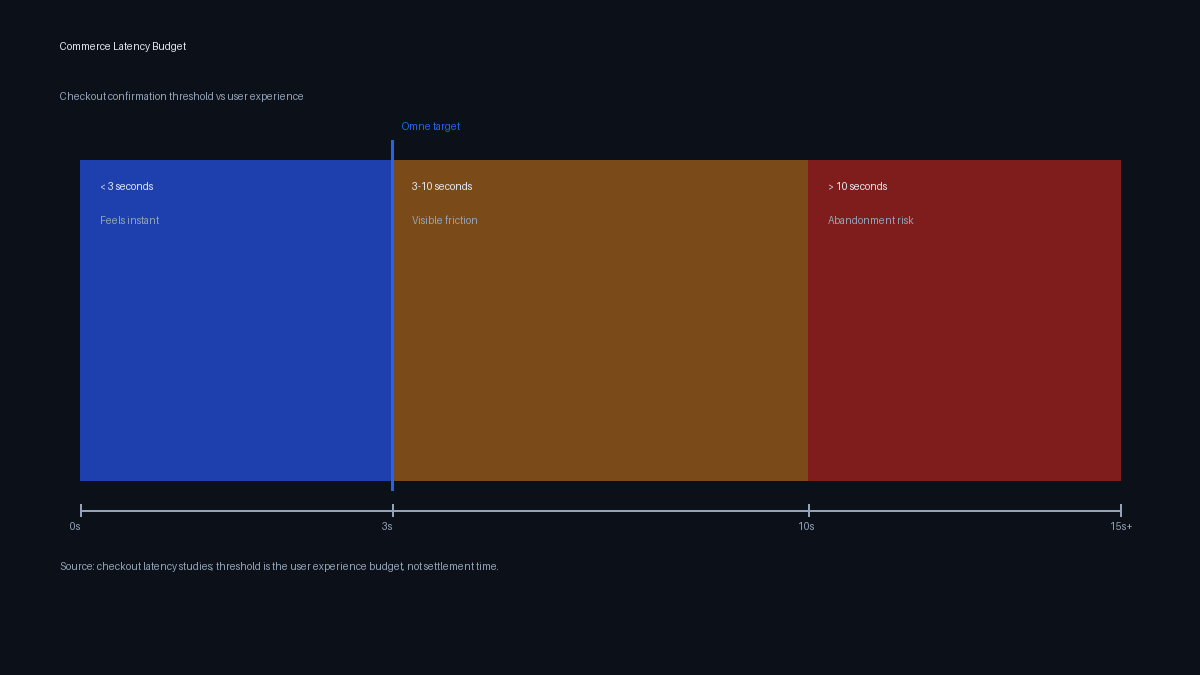

The Latency Budget for Commerce

Point-of-sale payments have a hard latency budget. Research from the Baymard Institute and payment processor SLAs converge on the same number: confirmation must arrive in under 3 seconds for a customer-facing payment flow to feel instant. Beyond 3 seconds, abandonment rates climb. Beyond 10 seconds, the experience is broken.

Here's where current options land for a merchant:

| Network | Finality | Merchant Cost | Settlement |

|---|---|---|---|

| Card networks (via processor) | ~1.8s authorization | 2.6--3.5% + per-tx fees | T+1 to T+2 days |

| Ethereum | 12--15s (single block) | $1--$50+ gas | Immediate (on-chain) |

| Solana | ~400ms slot / 6--12s confirmation | $0.00025 (spikes to $0.10+) | Immediate (on-chain) |

| Avalanche | 1--2s (subnet) | $0.01--$1 | Immediate (on-chain) |

| Bitcoin | ~10 minutes | $1--$30 | Immediate (on-chain) |

The comparison reveals a gap in the market. Card networks deliver fast authorization — but at steep cost to merchants, with settlement delayed by days and access gated behind processor intermediaries. Blockchains eliminate intermediaries and settle instantly — but introduce latency, volatile fees, or availability concerns. Neither side of the table delivers what commerce actually requires.

What the table doesn't show

Maria closes at 9 PM on a Friday. The register shows $847 in card sales. That money won't arrive in her bank account until Tuesday. Maybe Wednesday. Between now and then, she needs to pay her produce supplier (cash on delivery, Saturday morning) and a gas bill that auto-debits Monday. She's float-financing her own business with money she already earned but can't touch.

This is the hidden cost of T+2 settlement — a timing mismatch that forces small operators to borrow against their own revenue. On a blockchain with immediate on-chain settlement, Friday revenue is in the wallet Friday night. No float. No timing gap.

That's not an optimization. That's a different relationship with money.

Why Commerce Is a Different Design Space

The challenge isn't awareness — blockchain engineers understand the latency requirement. The challenge is that most architectures make a fundamental tradeoff between finality speed and settlement security. Different chains have optimized for different points on this spectrum.

Fast-finality chains (Solana, Avalanche) achieve low latency with different finality models. Solana's ~400ms slot time uses optimistic confirmation, where transaction reordering remains possible under certain conditions. Avalanche subnets achieve sub-second consensus but run as separate infrastructure from the main chain.

Security-first chains (Ethereum, Bitcoin) achieve strong finality with longer confirmation times. Ethereum's proof-of-stake delivers ~12-second blocks with robust security guarantees. Bitcoin provides the gold standard for settlement finality at ~10-minute cadence. Both were designed for security and censorship resistance — different priorities than point-of-sale speed.

The conventional wisdom has been that you choose fast confirmation or settlement-grade security — not both.

But ask the merchant behind the register: she needs the customer out the door in three seconds and she needs the settlement to hold up when her accountant reconciles on Monday. These aren't competing requirements — they're the same requirement, viewed from two different time horizons.

The Dual-Layer Architecture

Omne's central hypothesis is that this is a false dilemma. Commerce finality and settlement security can coexist if you separate them into two parallel block cadences within a single chain:

Commerce layer --- 3-second blocks. Every transaction achieves probabilistic finality within a single commerce round. For a merchant processing a latte, this is the only layer that matters: the customer gets confirmation before they leave the counter.

Security layer --- 9-minute blocks. Every 180 commerce blocks are rolled up into a single security block containing a cryptographic commitment (SHA-256 state root, execution trace hash, gas budget report). This provides Bitcoin-class settlement finality for high-value use cases, cross-chain bridges, and validator rotation.

The math is clean:

A merchant gets 3-second finality. A cross-chain bridge gets 9-minute settlement. Both properties exist on the same chain, with the same validators, using the same token.

Why Fees Must Be Microscopic — by Design, Not Promotion

Here is the thing nobody in crypto wants to say out loud: most blockchains are expensive on purpose. Gas fees on Ethereum aren't a bug — they're a market-clearing mechanism for scarce block space. When the network is busy, fees spike because that's how the protocol rations access. On a bad day, it prices out everyone except whales and MEV bots.

For a merchant, this is disqualifying. You cannot run a point-of-sale system on a network where the cost of a transaction is unknown until the moment you submit it.

Fees have to be structurally low --- not temporarily subsidized, not "low for now," but economically guaranteed to remain microscopic as a permanent architectural property.

A $4.50 coffee cannot bear a $3--4 transaction fee --- yet that is exactly what Ethereum charges for a simple transfer during moderate congestion. At Omne's base gas price of 20 micro-quar per unit of gas, a simple transfer costs approximately:

That's a tenth of a cent. Commerce-layer transactions receive an additional 50% fee reduction, bringing the effective cost below half a cent even for complex contract interactions.

This is not a promotional rate. Omne's fee model is structurally non-extractive:

- No fee auction. The base fee adjusts dynamically based on block utilization (target: 50%), clamped to a range of 1–100 micro-quar per unit of gas. It never enters an unbounded auction.

- Fee recycling. 92% of transaction fees are recycled to validators as income. Only 8% is burned for anti-spam deterrence. This preserves the OMC commerce token's soft dollar peg.

- Revenue cross-subsidization. 30% of compute revenue from the Omne Orchestration Network (OON) subsidizes on-chain transaction fees, creating a sustainable funding mechanism that doesn't rely on inflation.

What This Actually Changes

Consider a small e-commerce platform processing 10,000 transactions per day. On a high-fee L1 at $2 per transaction, that's $20,000/day --- $7.3 million per year. That $7.3 million doesn't build anything. It doesn't hire anyone. It doesn't open a second location. It's rent — paid to intermediaries for the privilege of accepting money from customers who already want to pay.

On Omne, 10,000 transactions at $0.001 each is $10/day --- $3,650/year. With 3-second finality, the platform can use the blockchain as the primary payment rail, not a secondary one. No fallback required, because the chain is designed for commerce uptime, not speculative throughput.

The difference between "blockchain as experiment" and "blockchain as infrastructure" is this: when the fee is lower than the cost of thinking about the fee, merchants stop thinking about fees. That's the threshold where adoption becomes structural rather than speculative.

That's also the threshold where the question stops being "can my business afford to use this?" and starts being "why am I still paying the old rate?"

The Gap That Remains

We're not claiming Omne has solved everything. The devnet is live, the SDK is on npm, and 500+ tests pass. But the network is young, the validator set is small, and real-world throughput under adversarial conditions hasn't been stress-tested at scale.

What we are claiming is that the architecture is correct: separating commerce finality from security settlement, keeping fees at the cost floor rather than the market-clearing price, and cross-subsidizing from compute revenue instead of inflating the token supply. These are structural decisions, not optimization tricks.

If you're building a payment application, a point-of-sale integration, or an e-commerce platform that needs blockchain finality at Visa-competitive latency and cost, the architectural foundation exists.

The people building on Omne aren't doing it because blockchain is interesting. They're doing it because somewhere, a bakery owner is about to close her laptop, open DoorDash Manager, and stare at the same number she stared at last month — the gap between what she earned and what she kept.

That gap is the problem. The architecture is the answer.

Get started: Omne SDK on npm | Documentation | GitHub

Join the community: Discord